For as long as we can all remember, Melbourne real estate has been more about capital growth and less about annual return. Sure, a good rental income is nice, but the dinner party bragger never mentioned earning a 7.5% yield. They tended to boast more about how their property investment had doubled in value, as they paused breifly to wash down the duck confit with a Primitivo from Puglia.

But today, lead indicators like auction clearance rates are suggesting capital growth has stalled. The clearance rate across the combined capital cities has been under 60% for six of the last eight weeks. At their peak, auction clearance rates hit 80%. Enquiry is down and days on market is up.

Traditionally, when people invest in real estate they expect a good stable income with strong capital growth. While capital growth is not pulling its weight right now, in many cities including Melbourne, the rental income (or annual return) is doing most of the heavy lifting.

This is bringing a property’s rental return including all the costs and risks sharply into focus and the investment equation has changed.

As discussed in our earlier article from February this year, Annual Return vs Capital Growth, the market appeared to be shifting toward a period where annual income return would become increasingly important for investors. Only 3 or 4 months later, that trend is becoming more entrenched.

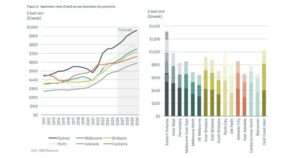

Recent research from Cotality (formerly CoreLogic) shows rental growth continuing to outperform dwelling value growth across large parts of the market. Particularly within Melbourne’s apartment sector, where prices have remained comparatively subdued against other capital cities.

Their recent Housing Chart Pack highlights the narrowing gap between renting and buying as rents continue rising faster than property values.

In Melbourne, rental growth was 4.5% annually to April ’26 whereas dwelling values fell by 0.6%. That may represent a big psychological shift for investors who purchased property some years ago expecting strong capital growth and a moderate rental return.

Today, many investors own assets producing stronger rental income but lower capital appreciation. While the total return may have been maintained the return profile has effectively inverted.

It can take time to recalibrate the initial investment expectations with reality. In a higher interest rate and higher cost-of-living environment, cashflow suddenly matters far more than it did during the ultra-low-rate years.

An investment generating above average returns is the new hero.

In April 2025 we analysed apartment investment returns showing many sales with gross yields of between 6.21% and 9.73%. As rents have continued to grow these yields are getting better and more commonplace.

This shift in focus to annual return is also changing the way apartments are being viewed relative to houses.

Traditionally, Melbourne houses have enjoyed significantly stronger capital growth due to the underlying land component and scarcity value. Apartments, by comparison, often lagged in price appreciation.

However, apartments are now producing materially stronger rental yields than houses across many parts of Melbourne. They certainly attract less land tax boosting their comparative net return.

Recent commentary from realestate.com.au highlights the growing affordability gap between houses and apartments, while rental demand for well-located units remains extremely strong.

That is creating a different type of investment proposition.

Houses may still ultimately outperform apartments from a long-term capital growth perspective. But in the current environment apartments are increasingly offering:

- lower entry prices,

- stronger rental return,

- improved cashflow,

- and lower overall holding risk.

Melbourne apartments are beginning to behave more like strong yielding, stable income producing investments. In the current economic climate, that’s pretty attractive.

Land tax, increased compliance obligations and rising interest rates have also forced investors to become much more conscious of holding costs. A decade ago, investors may have tolerated a lower cashflow because Melbourne prices were rising rapidly. Today investors need their investment property to throw off a meaningful income.

Perhaps the property investment conversation is changing to how smart investors are generating strong cash flow returns while capital growth takes a breather.